I’ve analyzed the most important area stage visibility shifts in Sistrix for the US and UK throughout the Could 2026 Core Replace, with a measured window from Could 26 to June 2, 2026. The rollout itself befell from Could 21 to June 2.

One of many clearest patterns I’ve discovered when going by way of the winners and losers was that visibility typically shifted towards the supply kind that appeared like a stronger match for the dominant intent, person market, and anticipated end result format of every question set: extra canonical, extra native, extra task-complete, or higher aligned with what customers have been possible searching for.

That is what I’d describe as an intent-destination reset, a helpful angle to grasp why some extremely authoritative domains misplaced, why some aggregators gained whereas others dropped, and why a broad “UGC misplaced” conclusion can be too simplistic.

The patterns that stood out most:

- Canonical reference manufacturers gained whereas pronunciation instruments, language Q&A websites and dictionary aggregators have been extra uncovered.

- UK ecommerce and market visibility shifted strongly towards local-market entities within the UK index.

- Class defining jobs and journey marketplaces gained, exhibiting that “aggregators misplaced” is just too easy.

- Discussion board, Q&A and open publishing surfaces declined, whereas giant social, video and visible platforms have been combined to optimistic.

- Well being and YMYL visibility break up by supply confidence and end result match, somewhat than by vertical alone.

In contrast with the March 2026 Core Replace, the place visibility appeared to consolidate away from many middleman, listing, broad aggregator and quick-answer layers towards stronger locations, Could seems like a extra exact recalibration of which vacation spot kind Google prefers for every intent and market.

Some March losers recovered in Could after they have been class defining activity locations, particularly in jobs and journey. Some March winners or secure authority sources slipped after they have been not the most effective supply kind for the dominant intent, and Could added a stronger localization sign, particularly round native market ecommerce entities within the UK.

Total, the clearest takeaway is that the Could 2026 Core Replace seems to have concentrated visibility round stronger default locations for every question’s intent, market, and anticipated end result kind.

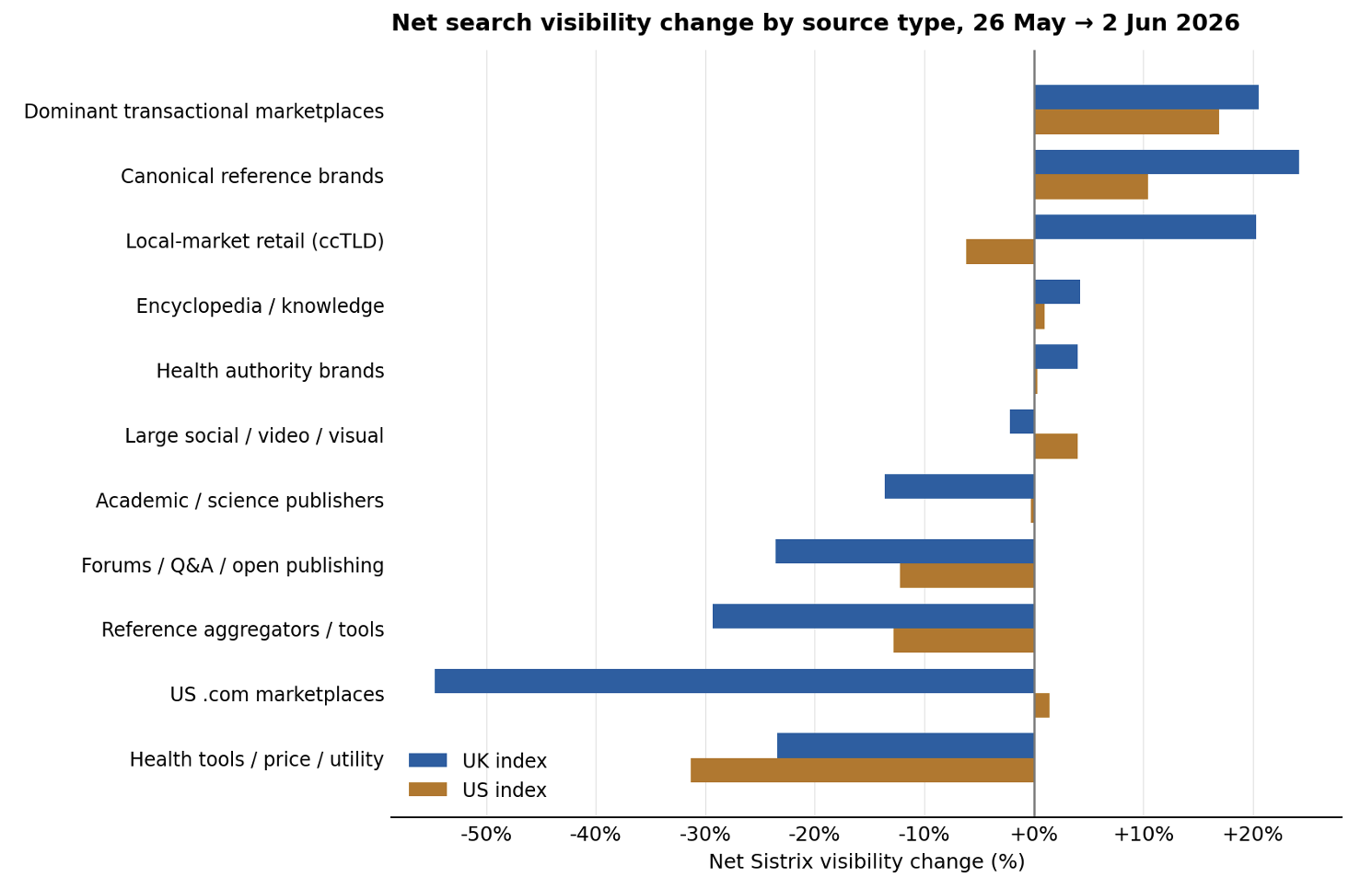

Determine 1. Internet Sistrix visibility change by supply kind, UK vs US. The “US .com marketplaces” bar reveals the localization mirror: they dropped sharply within the UK index, whereas holding within the US.

Let’s undergo the most important shifts by supply kind and market.

1. Supply kind match mattered greater than authority alone

Authority nonetheless mattered, however it didn’t clarify the total image: A number of extremely authoritative domains misplaced floor within the measured window, together with nytimes.com, springer.com, nature.com, who.int, census.gov and nih.gov.

We have to cease benchmarking on authority within the summary. For every precedence question cluster, establish the end result kind Google rewards now: definition, explainer, product class, market, official supply, native end result, video, device, comparability — then verify your rating web page genuinely IS that kind, not a close to match a stronger supply already owns.

Reference is the clearest instance as a result of the question universe overlaps closely: comparable intents, reverse outcomes. Aggregated, canonical reference manufacturers gained +24% within the UK and +10% within the US, whereas reference aggregators and instruments fell -29% and -13%. The vertical didn’t win or lose as a complete; Google seems to have favored a special anticipated supply kind.

| Area (UK index) | Change | Interpretation |

|---|---|---|

| cambridge.org | +40.9% | Canonical reference model (UK) |

| thesaurus.com | +39.7% | Canonical reference model (UK) |

| merriam-webster.com | +33.3% | Canonical reference model (UK) |

| youglish.com | -69.6% | Pronunciation utility layer |

| forvo.com | -68.1% | Pronunciation aggregator |

| hinative.com | -62.9% | Language Q&A device |

| onelook.com | -36.5% | Dictionary aggregator |

| wordreference.com | -35.0% | Secondary reference / discussion board layer |

The identical logic reveals up past definitions: genius.com held whereas lyric aggregators letras.mus.br (−49%) and lyrics.my (−43%) fell, and sciencedirect.com held whereas the scientific publishers above declined.

The helpful query isn’t solely “is that this area authoritative?”, however it’s “is that this the anticipated supply kind for the question after the replace?”

2. Discussion board and Q&A visibility contracted, whereas social/video platforms have been combined to optimistic

The pullback in discussion board, Q&A and open-publishing surfaces was clear: aggregated -24% within the UK and -12% within the US. Reddit, Quora and StackExchange all declined in each markets. Reddit’s share drop was smaller than some others, however its absolute motion was big: roughly 408 visibility factors misplaced within the UK and 361 within the US, as a result of it sits among the many highest-visibility domains within the index.

That is particularly related as a result of boards – Reddit above all – have been structurally boosted by way of Google’s Useful Content material period and the “hidden gems” / first-hand-experience push of 2023-2024. That is the primary replace shortly the place that publicity visibly contracted. Whether or not it is a sturdy correction or end-of-rollout volatility is among the major patterns to re-check.

This was not a broad UGC decline. When the surfaces are separated, giant social, video and visible platforms have been flat to optimistic total: aggregated +4% within the US and roughly flat (-2%) within the UK. YouTube, X and Fb gained within the US; Pinterest and Fandom gained in each markets. Completely different format, totally different person expectation, totally different end result.

| Area | Change | Floor kind |

|---|---|---|

| stackexchange.com | -31.8% | Discussion board/Q&A; US -18.3% |

| quora.com | -31.3% | Q&A; US -10.3% |

| reddit.com | -23.8% | Discussion board; US -13.7% (~408 / ~361 pts misplaced) |

| linkedin.com | -19.5% | Open publishing/profiles (UK); US flat |

| x.com | +14.5% | Giant social (US) |

| pinterest.com | +9.7% | Visible (US +9.7% / UK +10.6%) |

| fandom.com | +5.6% | Neighborhood/visible (US +5.6% / UK +10.2%) |

If discussion board type or skinny open publishing pages misplaced floor verify whether or not Google modified the popular end result format. If the SERP now favors video, visible, official sources or canonical references, the problem is competing in that format.

3. UK ecommerce visibility shifted towards native market entities

This was probably the most actionable worldwide search engine optimisation patterns.

The UK index reveals a transparent rebalancing of ecommerce and market SERPs towards native market entities and away from the .com model of the identical model. Native-market (ccTLD) retail rose +20% within the UK; US .com marketplaces fell −55% there.

The mirror holds within the US, the place these .com domains are roughly flat and UK ccTLDs edge down, which is strictly what you’d anticipate if market match, not the area itself, is the lever.

| Area (UK index) | Change | Interpretation |

|---|---|---|

| amazon.co.uk | +21.3% | Native-market entity favoured in UK |

| ebay.co.uk | +22.6% | Native-market entity favoured in UK |

| screwfix.com | +25.2% | UK retailer |

| amazon.com | -54.6% | US .com demoted within the UK index |

| walmart.com | -59.5% | Non-local market for UK customers |

| ebay.com | -53.7% | US .com demoted within the UK index |

| alibaba.com | -55.3% | Non-local market for UK customers |

For worldwide ecommerce, audit wrong-market rating, hreflang and canonical consistency, native entity readability, and nation particular alerts: stock, foreign money, pricing, transport, returns, native evaluations and assist.

The query Google appears to be answering: is the native web page genuinely the most effective end result for customers in that market?

4. Jobs and journey marketplaces present why “aggregators misplaced” is just too easy

Jobs and journey are the clearest counterexample to a easy “aggregators misplaced” interpretation.

Class defining transactional marketplaces gained in each markets – aggregated +21% within the UK and +17% within the US – whereas the informational and utility-style aggregators fell. The excellence isn’t aggregator vs non-aggregator. It’s main activity vacation spot vs by-product layer: the place customers can full the duty, versus one other layer summarizing it.

| Profitable transactional vacation spot | Change | Why it suits |

|---|---|---|

| journey.com | +82.2% | ravel market (US); UK +33.9% |

| skyscanner.com | +47.1% | Journey meta-search (US) |

| ziprecruiter.com | +44.8% | Jobs market (US) |

| expedia.co.uk | +38.1% | Journey OTA (UK); US +23.2% |

| glassdoor.com | +36.6% | Jobs/analysis vacation spot (US) |

| certainly.com | +25.9% | Jobs (UK +26% / US +24%) |

| reserving.com | +15.4% | Lodging market (UK +15% / US +13%) |

In case your mannequin aggregates data, benchmark in opposition to the websites that gained: are you the place customers full the duty, or a layer summarising it? That is most pressing for affiliate, comparability, reference and power websites: a by-product layer now wants a a lot stronger cause to exist within the SERP.

5. Well being was sorted by confidence and end result match

Well being didn’t win or lose as a vertical, it break up by supply confidence AND end result match.

Trusted well being locations typically held or rose: webmd.com +8.8% UK / +5.7% US, with Cleveland Clinic, Healthline and NHS broadly stable-to-positive.

On the similar time GoodRx and UbieHealth fell sharply, particularly within the UK, and even authority sources slipped (who.int −9.3% UK / −12.5% US; nih.gov down in each).

The reinforcement of the core thesis: belief is critical in YMYL, however most popular web page kind and question intent nonetheless determine the result. A worldwide authority web page, a symptom checker, a drug-price device and a patient-friendly explainer will not be interchangeable outcomes.

| Area | Change | Kind / interpretation |

|---|---|---|

| goodrx.com | -80.0% | Drug-price utility (UK); US -17.5% |

| ubiehealth.com | -38.8% | Symptom-checker utility; US -38.9% |

| webmd.com | +8.8% | Trusted well being vacation spot; US +5.7% |

| who.int | -9.3% | Authority nonetheless uncovered on intent combine; US -12.5% |

| nih.gov | -7.5% | Broadly secure; US -0.8% |

For YMYL, don’t cease at E-E-A-T alerts and creator bios. Validate whether or not affected queries now want a special supply kind, whether or not official steering, patient-friendly explainers, medical establishments, instruments, native providers or brisker information, and whether or not your format nonetheless matches.

The underside line

The Could 2026 Core Replace seems like a recalibration of which supply kind Google treats because the default vacation spot for every intent. Canonical reference manufacturers, local-market ecommerce entities and category-defining transactional marketplaces gained within the clearest examples. Boards/Q&A, mistaken market domains, by-product informational instruments and decrease confidence utility layers have been probably the most uncovered.

It means probably the most helpful query after this replace is: for this question, on this market, on this end result format – is my web page nonetheless the most effective default vacation spot?

{kind=link}